If you are a freelancer, independent contractor, or small business owner, there comes a point where being a sole proprietor might not be the most efficient structure for your growing business.

Many entrepreneurs reach a stage where they start wondering if it is time to incorporate and be taxed as an S corporation (often called an “S-Corp”). The switch can lead to significant tax savings and added legal protection, but it is not for everyone.

Here’s how S corporations work, what benefits they offer, what trade-offs to expect, and when the switch might make sense for you.

Why S-Corps Can Save You Money

1. Self-Employment Tax Savings

As a sole proprietor, you pay a 15.3% self-employment tax (which includes Social Security and Medicare) on your entire net income.

S corporations allow you to divide your income into two parts:

- A reasonable salary (which is subject to Social Security and Medicare taxes), and

- Distributions (which are subject to income tax, but not to payroll taxes).

By splitting your income, you can reduce the amount subject to self-employment taxes.

Example:

If you earn $120,000 as a consultant:

- As a sole proprietor, you would pay self-employment tax on the full $120,000 (around $18,000).

- As an S-Corp, if you paid yourself a $60,000 salary, you would pay payroll taxes on that amount only (around $9,200).

That could mean roughly $9,000 in tax savings each year.

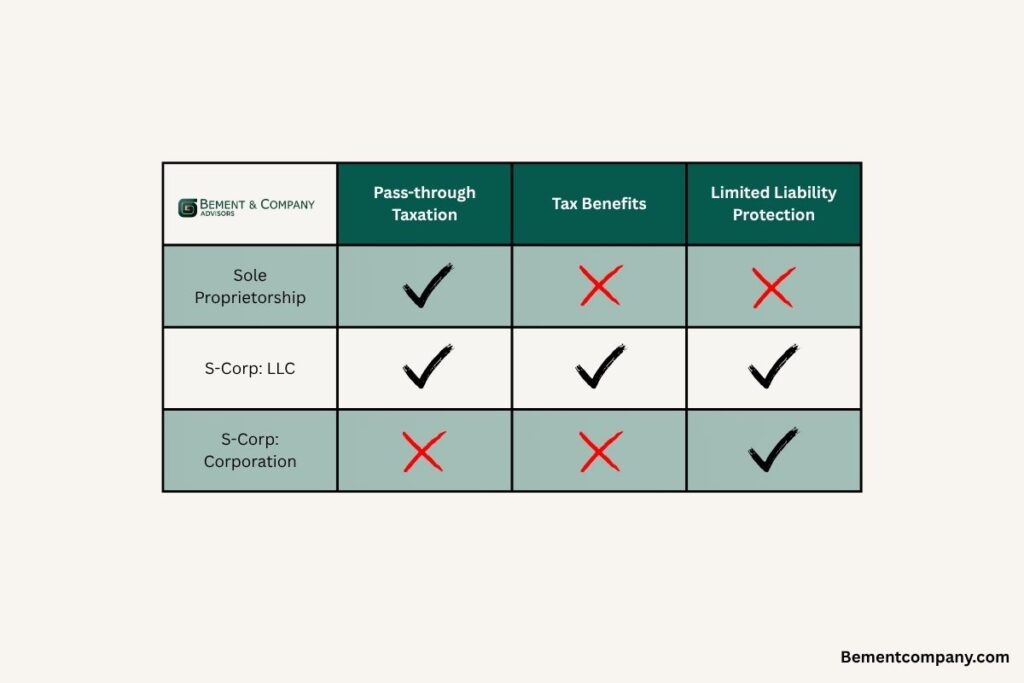

2. Pass-Through Taxation

Like a sole proprietorship, an S-Corp is a pass-through entity, meaning profits and losses pass through to your personal tax return. The business itself does not pay federal income tax.

This avoids the double taxation that applies to C corporations, where profits are taxed both at the corporate level and again when distributed to shareholders.

3. Legal Protection

An S-Corp can help protect your personal assets from business liabilities.

If a client or customer files a claim against your business, your personal savings, home, and other assets may be shielded from business-related legal actions.

This protection is not absolute, but it adds a meaningful layer of separation between you and your business.

Learn more about business structure protection from the U.S. Small Business Administration.

Trade-Offs to Consider Before Switching

While the tax savings can be appealing, S-Corps come with more administrative responsibilities and costs than sole proprietorships.

Here are some key trade-offs:

1. Payroll Requirements

Even if you are the only employee, you must run payroll, withhold taxes, and file regular payroll tax reports.

Most S-Corp owners use a payroll service such as Gusto, QuickBooks, or ADP to handle this.

2. Separate Tax Filings

S corporations must file a separate Form 1120-S business tax return by March 15 each year, in addition to your personal return.

This typically requires the help of an accountant or tax preparer.

3. Reasonable Salary Rules

The IRS requires you to pay yourself a fair market wage for the work you perform.

Paying yourself too little to avoid payroll taxes can trigger IRS penalties.

4. State-Level Fees

Some states require annual filing fees, minimum taxes, or franchise taxes for S corporations, even if your income is low.

For example, California has a minimum franchise tax of $800.

5. Professional Fees

Many S-Corp owners hire accountants or bookkeepers to manage their records and payroll, which adds cost but also ensures compliance.

Bement & Company offers both tax preparation and bookkeeping services.

For more information on the benefits of converting to an S-Corp, listen to our Wealth Game Podcast Episode

When It Makes Sense to Switch

A good rule of thumb:

Switching to an S-Corp becomes worthwhile once your net income (after expenses) reaches $75,000–$100,000 per year.

That is typically the point where the tax savings outweigh the added administrative costs.

Example:

- If you make $120,000 as a sole proprietor, you might save $9,000 annually in taxes by switching.

- But if you make $40,000, the cost of payroll, bookkeeping, and tax filings might eat up the savings.

If you expect your income to continue growing, it may make sense to incorporate sooner rather than later to start realizing those tax savings.

How to Make the Switch

- Form an LLC or Corporation in your state (consult your accountant or legal advisor for the best choice).

- Elect S-Corp status by filing Form 2553 with the IRS.

- The form must be filed within two months and 15 days after the beginning of the tax year you want the election to take effect.

- Set up payroll for yourself and any other employees.

- Work with a CPA or payroll provider, like Bement & Company, to handle quarterly filings and ensure compliance.

Final Thoughts

Switching from a sole proprietorship to an S-Corp can offer meaningful tax savings, liability protection, and a more professional structure for your growing business.

But it is not a one-size-fits-all solution. The best approach is to review your financials annually with a tax strategist or CPA to ensure your business is organized in the most tax-efficient manner possible.

If you are considering making the switch or want to see if it would save you money, schedule a strategy session with Bement Company.