For most people, tax season feels like a frantic sprint to the finish line every April. But the most successful financial strategies are not built in a single month. They are built during the rest of the year when you still have time to make adjustments.

Since we are already well into 2026, now is the perfect time to review your situation. Tax planning is essentially a combination of how much you think you will make and where that money is coming from. This “income source” is the secret to a tax-effective result.

It is a common misconception that two people with the same total income will pay the same amount of taxes. In reality, their tax bills could look entirely different based on how they earned their money. Here is a simple, effective approach to building your 2026 plan.

Step 1: Take Inventory of Your Income Sources

Your tax strategy starts with a clear picture of your cash flow. Most income falls into a few core categories like wages from an employer, self-employment, or investment earnings.

Take a moment to look at your tax return from last year to see where your money came from. Then, consider any changes you expect for 2026. Other types of income you might have include:

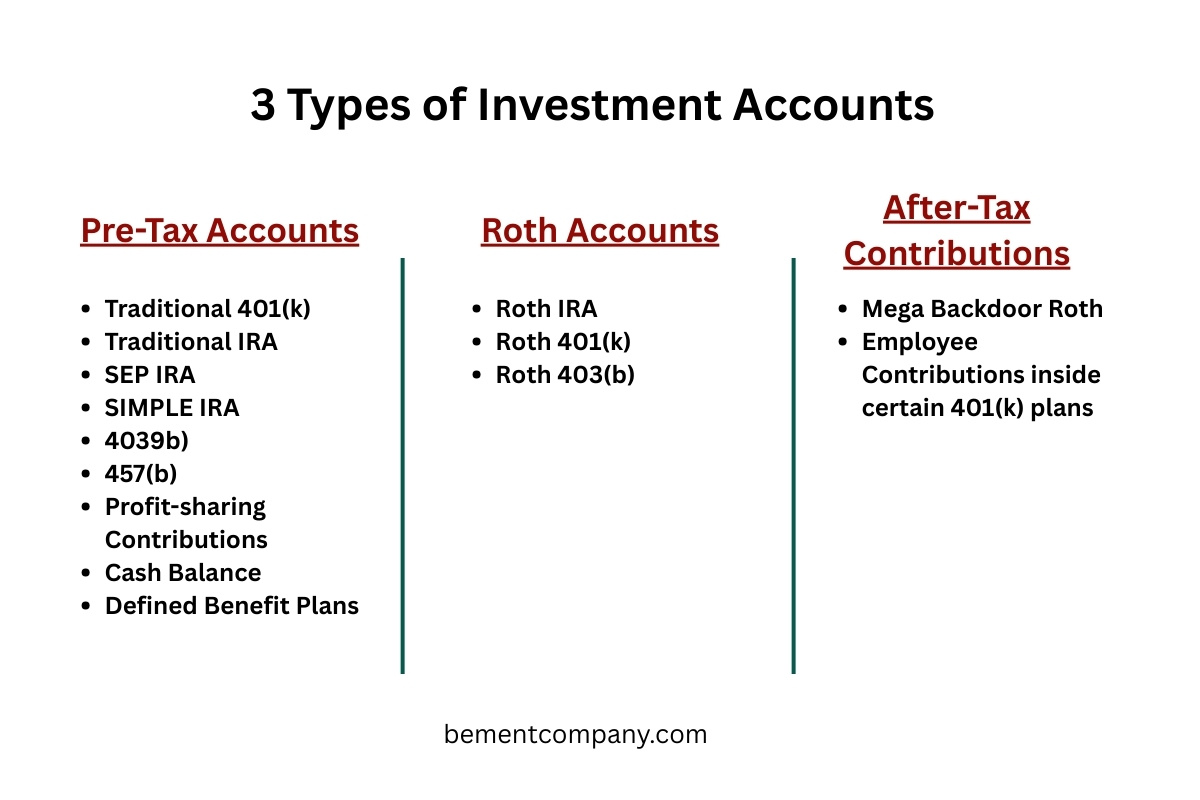

- Retirement income: Pensions, Social Security, or IRA and 401(k) withdrawals.

- Rental income: Earnings from real estate properties.

- Business distributions: Specifically for S-corp or partnership owners.

- Interest: Earnings from bonds or high-yield savings accounts.

If you are a business owner, you might even consider switching to an S-Corp if your income has reached a certain threshold. Knowing your sources is the first step toward keeping more of what you earn.

Step 2: Get Familiar With the Different Types of Taxes

Not all income is created equal in the eyes of the IRS. These differences can add up quickly, and understanding the “tax buckets” helps you avoid surprises.

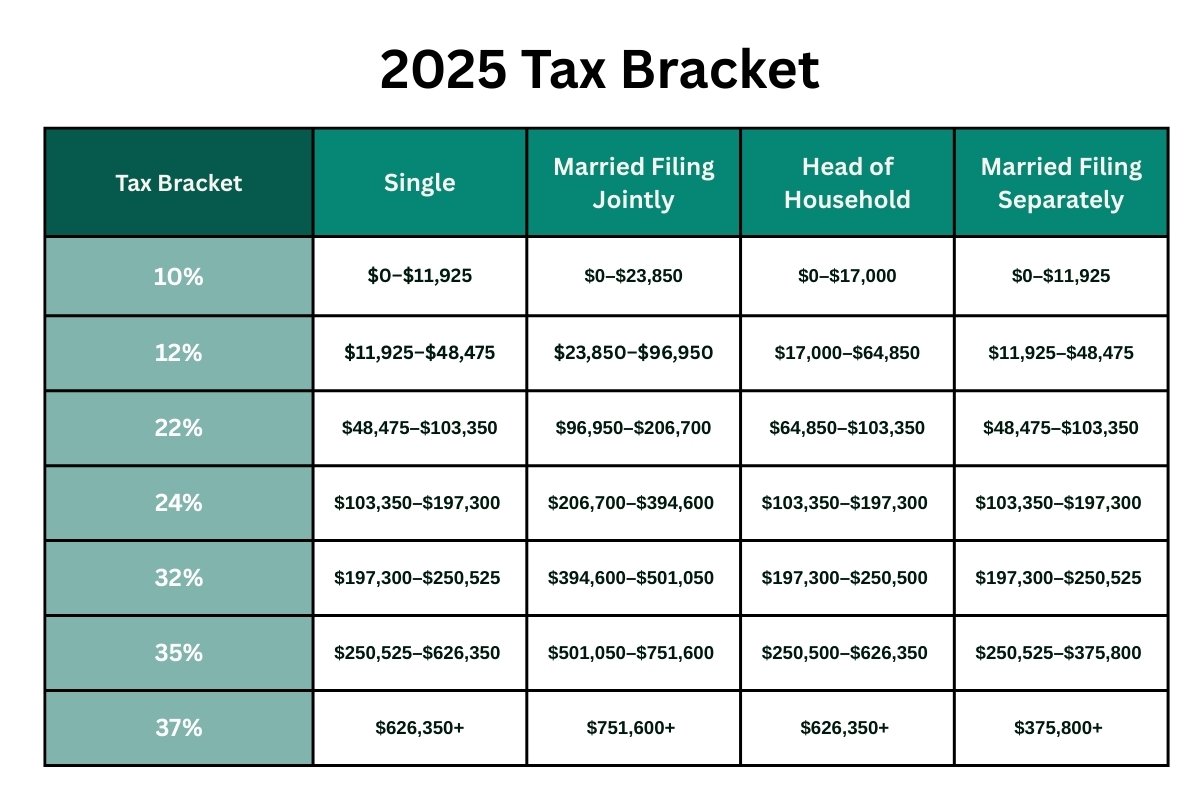

Wages and Progressive Rates

Wages are subject to a progressive income tax. According to the IRS tax brackets, these rates can range from 10% to 37%. It is vital to know the rate your next dollar of income will pay. Also, do not forget that wages are subject to payroll taxes, such as Social Security and Medicare, which total 7.65%.

Self-Employment and Freelance Income

This income is subject to the same progressive rates as wages. However, most freelance jobs do not automatically withhold taxes. You are also responsible for the full self-employment tax of 15.3%. This is why a proactive tax strategy is so important for the self-employed.

Investment Earnings

These can be subject to a variety of rates. Interest and short-term capital gains are usually taxed at ordinary rates up to 37%. However, qualified dividends and long-term capital gains often enjoy lower rates between 0% and 20%, depending on your total income.

Retirement and Rental Income

Retirement income may be fully taxable, partially taxable, or even tax-free, such as certain Roth distributions. Rental income is generally taxed at ordinary rates, though you can often use deductions to decrease the total taxable amount.

Step 3: Strategies to Manage Your Tax Burden

Once you know where your money is coming from and how it is taxed, you can take action.

Align your tax payments with your earnings. If a growing portion of your income comes from somewhere outside a traditional W-2 job, withholding alone might not be enough. Freelance, investment, or rental income often requires quarterly estimated tax payments to avoid IRS penalties.

Use withholding and estimates together. If your income is uneven, you can adjust your paycheck withholding to pair it with your estimated payments. This keeps your cash flow steady and prevents a massive bill next April.

Be intentional about timing. Sometimes you have control over when you receive income or pay expenses. If you are self-employed, you might choose to delay an invoice or prepay a 2027 expense to smooth out your tax bill.

Check your plan throughout the year. Your income mix can change quickly. A 10-minute review in the summer or fall can help you stay on track. Small updates now make a big difference later.

Final Thoughts

Understanding your income sources is the foundation of a smart 2026 tax plan. By aligning your payment strategies and being intentional about your timing, you turn tax season into a strategic advantage instead of a yearly stress point.

If you want a professional eye to help you find “tax leaks” or build a personalized plan, Bement & Company is here to help. Taking a few extra minutes today will save you time, money, and frustration when it is time to file.