Investment accounts can feel overwhelming fast. The terminology matters. The rules overlap. And the tax consequences of getting it wrong can follow you for decades.

Today we are breaking it all down in plain English. This guide covers how the most common investment accounts work, how they are taxed, what strategies high earners use to get the most out of them, and which moves you can still make before the April 15 tax deadline.

If you want more control over when and how you pay taxes, this is where it starts.

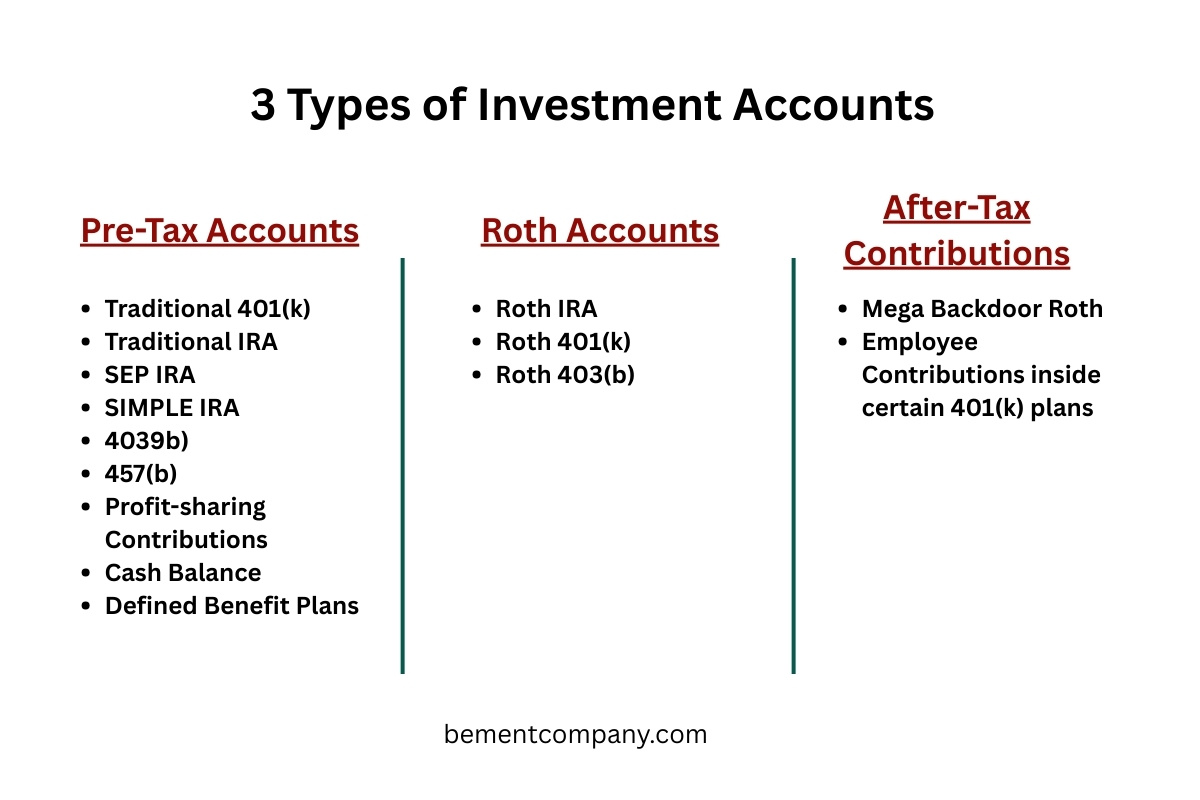

Three Tax Categories for Investment Accounts

Nearly every tax-advantaged investment account fits into one of three tax categories. Think of these as different tools in your tax toolbox.

Pay Tax Later (Pre Tax Accounts)

These accounts give you a tax benefit today. You generally reduce your taxable income now and pay taxes later when you withdraw the money.

Common examples include:

- Traditional 401(k)

- Traditional IRA

- SEP IRA

- SIMPLE IRA

- 403(b)

- 457(b)

- Profit-sharing contributions

- Cash balance and defined benefit plans

These accounts are powerful when your current tax rate is high, and you want immediate relief.

Pay Tax Now (Roth Accounts)

With Roth accounts, you pay taxes today in exchange for tax-free growth and tax-free withdrawals later.

Common examples include:

- Roth IRA

- Roth 401(k)

- Roth 403(b)

Roth accounts create a tax-free pool of money for the future. This flexibility becomes extremely valuable in retirement or during years when you want to control your taxable income.

Pay Tax Now With a Twist (After Tax Contributions)

After tax contributions are not Roth contributions, but they can often be converted into Roth with the right plan structure.

The most common example is after-tax employee contributions inside certain 401(k) plans. This is where strategies like the Mega Backdoor Roth come into play.

If you only remember one thing:

- Pre-tax helps reduce taxes today

- Roth helps reduce taxes later

- After tax can be a bridge to Roth

The Main Types of Investment Accounts

Employer-Sponsored Plans

These are usually the biggest drivers of tax savings for high earners.

Common employer plans include:

- 401(k)

- 403(b)

- 457(b)

- SEP IRA

- SIMPLE IRA

- Solo 401(k)

- Defined benefit or cash balance plans

Employer plans often allow much higher contribution limits than individual accounts, especially for business owners.

Individual Accounts

These are accounts you open on your own, outside of an employer.

- Traditional IRA

- Roth IRA

While contribution limits are lower, these accounts play a key role in tax diversification and cleanup planning after year-end.

Health and Education Accounts

These are often overlooked but incredibly powerful when used correctly.

- Health Savings Account

- Flexible Spending Account

- 529 education plans

HSAs, in particular, offer a rare triple tax benefit: deductions going in, tax-free growth, and tax-free withdrawals for medical expenses.

Tax Friendly Accounts

These are not tax advantaged, but they still matter.

- Taxable brokerage accounts

- Municipal bonds

Taxable accounts provide flexibility, capital gains treatment, and liquidity that retirement accounts do not.

How These Accounts Are Taxed

Pre Tax Accounts

What to know:

- Contributions often reduce taxable income

- Growth is tax-deferred

- Withdrawals are taxed as ordinary income

- Required minimum distributions apply later in life

These accounts work best when you expect your tax rate to be lower in the future or when you need tax relief today.

Roth Accounts

What to know:

- Contributions are made after tax

- Growth can be tax-free

- Qualified withdrawals are tax-free

- Roth IRAs do not have required minimum distributions during your lifetime

This makes Roth accounts ideal for long-term planning and estate strategies.

After Tax Contributions

What to know:

- Contributions are already taxed

- Growth is taxable unless converted

- The value comes from converting to Roth

Not every plan allows this, which is why reviewing plan features is critical.

The Three Contribution Sleeves Inside Employer Plans

If you have a 401(k), there are usually three places money can go.

Employee Contributions

These come directly from your paycheck.

- Can be pre-tax or Roth

- Must generally be made by December 31

This is usually the first lever people pull.

Employer Contributions

These include matches and profit sharing.

- Almost always pre-tax

- Often can be made after year-end

For business owners, this sleeve creates major planning opportunities.

After Tax Employee Contributions

This is different from Roth.

- Not all plans allow it

- Can unlock Mega Backdoor Roth strategies

If your plan allows after-tax contributions and Roth conversions, this can be one of the most powerful tools available.

What You Can Still Do After December 31

Some contributions can still be made after year-end and count for the prior tax year.

These usually include:

- Traditional IRA contributions

- Roth IRA contributions

- SEP IRA contributions

These accounts follow the tax filing deadline, usually April 15.

However, employee deferrals tied to payroll must generally be completed by December 31. This includes 401(k), 403(b), and 457(b) deferrals.

Employer contributions are different and often remain available until the business filing deadline.

Key Tax Planning Strategies for High Earners

Fill the Best Buckets First

A common order:

- Get the full employer match

- Max your 401(k)

- Use an HSA if eligible

- Consider a Backdoor Roth IRA

- Explore Mega Backdoor Roth options

- Invest taxable assets tax efficiently

Roth vs Pre-Tax Is Not Guesswork

Many high earners intentionally use both.

- Pre-tax for current relief

- Roth for future flexibility

This is called tax diversification.

Backdoor Roth IRA

High earners can often:

- Make a non-deductible IRA contribution

- Convert it to Roth

Be careful if you have other pre-tax IRAs. The pro rata rule can create unexpected taxes.

Mega Backdoor Roth

If your 401(k) allows:

- After tax contributions

- In plan Roth conversions or rollovers

You may be able to move significantly more money into Roth than most people realize.

Business Owner Strategies

Retirement plans can become tax engines for business owners.

- Solo 401(k)

- SEP IRA

- Cash balance plans

These should always be modeled. Copying someone else’s setup is a costly mistake.

Common Mistakes That Cost Real Money

- Confusing Roth with after-tax

- Missing contribution deadlines

- Not coordinating multiple accounts

- Ignoring tax consequences until later

Most penalties and missed opportunities come from lack of coordination, not lack of income.

A Simple Action Checklist

- Review your 401(k) elections

- Confirm you are getting the full employer match

- Ask HR about after tax and Roth conversion features

- Check if you can still make IRA or SEP contributions

- If you own a business, review whether your retirement plan matches your income level

Final Thoughts

Investment accounts are not just savings vehicles. They are tax tools.

Pre-tax accounts help you lower taxes today.

Roth accounts help you lower taxes later.

After tax contributions can unlock advanced strategies.

For high earners, the real win is not just saving for retirement. It is controlling when taxes are paid.

Stop using default settings. Build a strategy that matches your income, your goals, and your tax bracket.

That is how you turn investment accounts into a real advantage.