Saving for retirement is not a one-size-fits-all journey. Each stage of life comes with different priorities, pressures, and opportunities.

In your twenties, the focus is usually on building habits. In your thirties and forties, it shifts toward structure and growth. As you move into your fifties and sixties, the conversation becomes more about timing, income, and long-term sustainability.

The good news is that there is no perfect starting point. What matters is understanding what to focus on at each stage and making steady progress over time.

Let’s walk through retirement savings strategies by age so you can make smarter decisions no matter where you are today.

In Your Twenties: Build the Right Habits Early

Your twenties are less about large account balances and more about consistency.

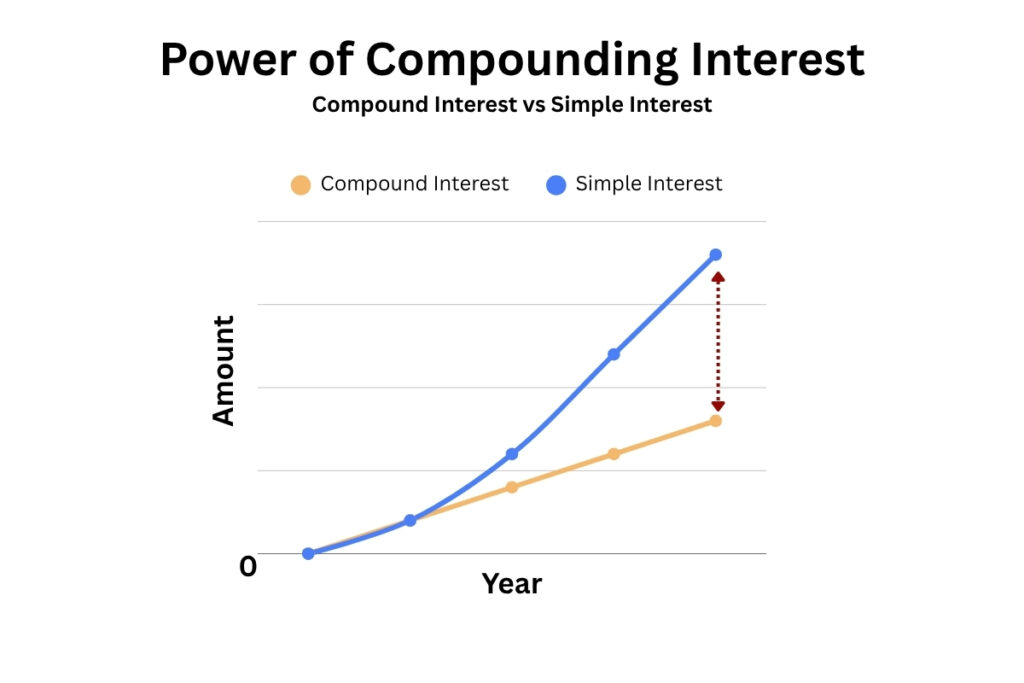

One of the biggest advantages you have in this decade is time. The earlier you start saving, the more you benefit from compound growth, which is when your investment earnings begin generating their own earnings over time.

At this stage, focus on:

- Building a consistent saving habit, even if the amount is small

- Contributing to employer-sponsored plans, like a 401(k) if available

- Taking advantage of employer matching contributions

- Learning basic investing concepts over time

- Treating retirement savings like a fixed monthly expense

The goal is momentum, not perfection

In Your Thirties: Add Structure and Intentionality

By your thirties, your income is often increasing, and your financial life becomes more complex. This is when retirement planning should become more intentional.

You may be balancing competing priorities like housing, family, and career growth. That makes it even more important to have a clear structure in place.

Focus areas during this decade include:

- Increasing contribution percentages as income grows

- Understanding how employer match programs work and maximizing them

- Managing debt and avoiding high-interest obligations

- Aligning lifestyle decisions with long-term financial goals

- Exploring additional income streams or career growth opportunities

This is the decade where small increases in contributions can have a large long-term impact. Check out Charles Schwab’s article for a comprehensive Savings Guide

In Your Forties: Take Inventory and Close the Gap

Your forties are often the turning point for retirement planning.

At this stage, you likely have a clearer picture of your financial situation. This is the time to evaluate whether you are on track and make adjustments if needed.

Focus on:

- Reviewing your current retirement balances

- Comparing projected retirement income to your expected needs

- Identifying gaps in savings

- Increasing contributions where possible

- Evaluating your investment allocation and risk exposure

- Reviewing your Social Security earnings record for accuracy

This is also a great time to look at your full financial picture. Retirement planning does not exist in isolation. It connects to your tax strategy, investments, and cash flow.

In Your Fifties and Sixties: Prepare for the Transition

As retirement approaches, the focus shifts from accumulation to planning for income and stability.

This is where decisions become more detailed and more important.

Key priorities include:

- Continuing to save aggressively where possible

- Taking advantage of catch-up contributions in retirement accounts

- Reducing or eliminating outstanding debt

- Planning when to begin Social Security benefits

- Understanding healthcare costs and insurance options

- Defining what retirement will actually look like

At this stage, clarity matters more than speed. The goal is to create a sustainable income plan.

Timeless Retirement Principles That Apply at Any Age

While priorities shift over time, some principles remain constant.

- Automate your savings whenever possible

- Avoid comparing your progress to others

- Revisit your plan periodically

- Focus on what you can control today

- Align your tax strategy with your retirement plan

Retirement planning is not just about saving. It is about creating flexibility and control over your future income.

Why Retirement Planning Is Also a Tax Strategy

One of the most overlooked parts of retirement planning is taxes.

Different accounts are taxed differently:

- Traditional 401(k) and IRA contributions may reduce taxes today, but are taxed later

- Roth accounts are funded with after-tax dollars but can grow tax-free

- Brokerage accounts are taxed differently depending on gains

Understanding how these accounts work together can help you control how and when you pay taxes in retirement. For more strategies on how to avoid penalties and taxes on retirement accounts, check out the Bement & Company blog post.

Final Thoughts

Retirement planning is not about following someone else’s timeline. It is about making the best decisions with the resources you have today.

Each decade brings different opportunities, but the core idea remains the same. Consistency, awareness, and intentional decisions drive long-term results.

Whether you are just starting out or approaching retirement, taking action today creates more options tomorrow.

If you want help aligning your retirement strategy with your tax plan and long-term financial goals, consider scheduling a strategy session with Bement Company.