When it comes to lowering your tax bill, two terms come up constantly: tax deductions and tax credits.

Many taxpayers assume they work the same way. In reality, they operate very differently. Understanding the difference can make a meaningful impact on how much you ultimately pay in taxes.

A tax deduction lowers the amount of income that is taxed. A tax credit directly lowers the amount of tax you owe.

Both can be valuable tools in tax planning, but tax credits are often more powerful because they reduce your tax bill dollar for dollar.

Let’s break down how each one works and look at some examples.

How Tax Deductions Work

A tax deduction reduces your taxable income. This means the deduction lowers the amount of income that the IRS uses to calculate your taxes.

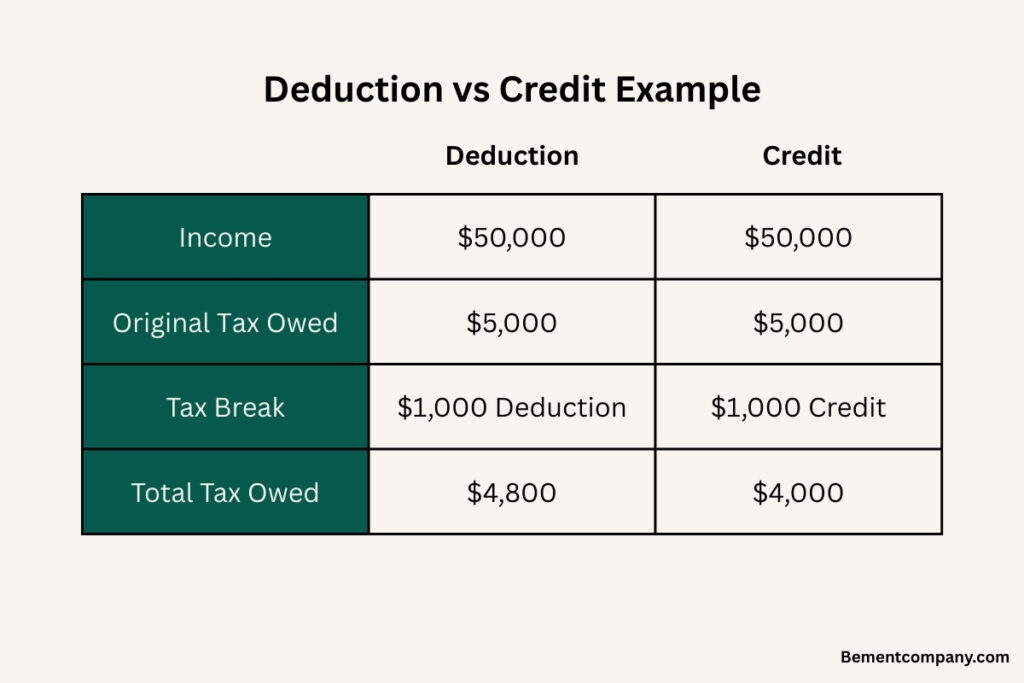

For example, imagine a single taxpayer earning $50,000 in taxable income who owes $5,000 in taxes.

If the taxpayer receives a $1,000 tax deduction, their taxable income decreases from $50,000 to $49,000. Because taxes are calculated based on income brackets, the deduction lowers the tax bill by only a portion of the deduction amount.

In this example, the tax bill decreases from $5,000 to approximately $4,800.

Result:

A $1,000 deduction saves about $200 in taxes.

Common examples of tax deductions include:

- Mortgage interest deductions

- Charitable contribution deductions

- Student loan interest deductions

- Business expense deductions

- Health Savings Account contributions

How Tax Credits Work

A tax credit works differently. Instead of lowering taxable income, it directly reduces the amount of tax owed.

Using the same example, imagine the taxpayer with a $5,000 tax bill receives a $1,000 tax credit.

Instead of reducing taxable income, the credit reduces the tax bill itself.

Result:

The tax bill drops from $5,000 to $4,000.

This means the full $1,000 credit lowers the tax owed by $1,000.

That is why tax credits are often considered more valuable than deductions.

Refundable vs Nonrefundable Tax Credits

Not all tax credits work the same way. Credits are generally divided into two categories.

Nonrefundable Credits

A nonrefundable credit can reduce your tax bill to zero, but it cannot create a refund beyond the taxes you owe.

Example:

If you owe $1,000 in taxes and have a $2,000 nonrefundable credit, the credit eliminates the $1,000 tax bill but the remaining $1,000 is not refunded.

Common nonrefundable credits include:

- Lifetime Learning Credit

- Child and Dependent Care Credit

- Adoption Credit

Refundable Credits

A refundable credit can create a refund even if you owe no tax.

Example:

If you owe $500 in taxes and qualify for a $2,000 refundable credit, the credit eliminates the $500 tax bill and the remaining $1,500 is refunded to you.

Examples of refundable credits include:

- Earned Income Tax Credit

- Additional Child Tax Credit

Common Tax Credits That Reduce Your Tax Bill

Several credits are commonly used by taxpayers depending on their situation.

Child Tax Credit

Families may claim up to $2,200 per qualifying child for the 2025 tax year, subject to income limits and eligibility rules.

The credit phases out for higher-income taxpayers and requires the child to meet several IRS criteria.

Earned Income Tax Credit

The Earned Income Tax Credit is designed to help lower-income and moderate-income workers.

The credit amount depends on income, filing status, and number of children. Because it is refundable, it can produce a refund even if the taxpayer owes little or no tax.

Education Tax Credits

Education credits help offset the cost of higher education.

The two most common credits are:

American Opportunity Tax Credit

Worth up to $2,500 per student for undergraduate education.

Lifetime Learning Credit

Worth up to $2,000 per tax return for qualified education expenses.

Why Understanding the Difference Matters

Knowing the difference between deductions and credits can help you make better tax planning decisions.

For example, two taxpayers may receive the same $1,000 benefit, but if one receives it as a deduction and the other receives it as a credit, the credit may provide significantly greater tax savings.

Understanding which deductions and credits apply to your situation allows you to reduce your tax liability more effectively.

Final Thoughts

Tax deductions and tax credits both help reduce the amount you pay in taxes, but they work in very different ways.

A tax deduction reduces taxable income. A tax credit directly reduces the tax bill itself.

Because of this difference, tax credits are often more powerful tools when available. However, credits typically come with eligibility rules, income limits, and other requirements.

Understanding these differences is an important step toward making informed tax planning decisions.

If you want to ensure you are taking advantage of both deductions and credits available to you, consider scheduling a tax planning session with the Bement Company strategy team.