The end of the year is the perfect time to review your finances and make sure you’re ready for tax season.

With several new tax rules arriving in 2026 and a few key updates already in effect for 2025, taking a proactive approach can save you both time and money.

Here’s what you need to know to stay ahead of upcoming tax changes, avoid filing headaches, and make the most of every deduction available to you.

Preparing to File Your 2025 Tax Return

Before you can plan for 2026, it’s important to wrap up 2025 the right way. These steps can make filing smoother, and may help you catch tax-saving opportunities early.

1. Gather Proof for Tip and Overtime Deductions

The One Big Beautiful Bill Act (OBBBA) introduced major tax breaks for workers who earn tips or overtime pay. Read our post for more information on the No Tax on Tips or No Tax on Overtime

- No Tax on Tips: You can deduct up to $25,000 in qualified tips ($50,000 if married filing jointly).

- No Tax on Overtime: Up to $12,500 in qualified overtime pay ($25,000 if filing jointly) can be excluded from taxable income.

Since employers are not yet required to include this information on W-2s or 1099s for 2025, you’ll need to track your own records. Keep pay stubs, employer confirmation letters, and any proof of these earnings to verify your deduction.

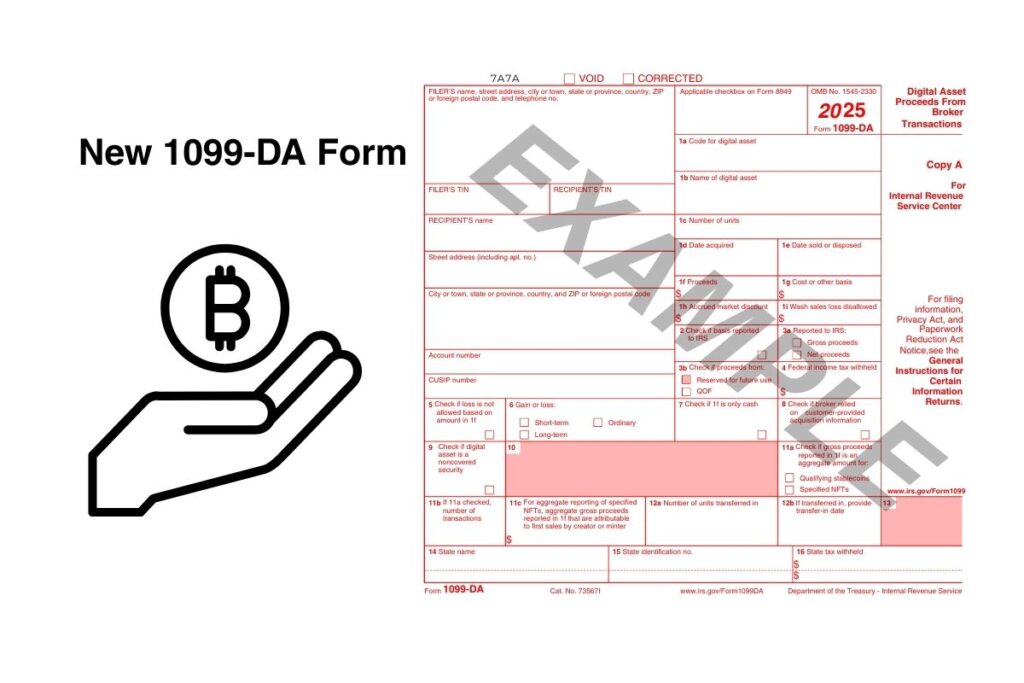

2. Watch for New Form 1099-DA (Digital Assets)

If you’ve traded cryptocurrency or other digital assets, expect to receive a new IRS form: Form 1099-DA.

Starting in 2025, exchanges and brokers must report digital asset transactions, including sales, exchanges, and transfers. To prepare:

- Track your cost basis (the original purchase amount).

- Record sale dates and transaction values.

- Keep a list of all wallets and exchanges you used.

Accurate tracking helps you avoid mismatches or IRS questions when filing your return.

3. Don’t Ignore 1099-K Forms

Form 1099-K is used by payment processors such as PayPal, Venmo, and Stripe to report business or side income.

The current federal threshold is 200 transactions and $20,000 in payments, but given the frequent changes in the law, you might still receive a form even if you didn’t meet those limits.

If you receive one in error, don’t discard it. Keep it with your tax documents. You or your accountant will need it to report your income correctly and prevent filing mismatches.

4. Review IRA and HSA Contributions

You have until April 15, 2026 (or your filing date, if earlier) to make 2025 contributions to your:

- Individual Retirement Account (IRA)

- Health Savings Account (HSA)

Contributions to these accounts are among the easiest ways to lower your taxable income while building long-term financial security.

What’s Changing in 2026

Looking ahead, several significant tax updates are scheduled to take effect in 2026. Knowing them now helps you plan your financial strategy over the next 12–18 months

1. Above-the-Line Charitable Deductions Return

Beginning in 2026, taxpayers can deduct charitable contributions even if they don’t itemize deductions:

- $1,000 for single filers

- $2,000 for joint filers

A 0.5% floor will also apply to itemized charitable deductions, meaning only donations above that threshold can be deducted.

2. Itemized Deduction Phaseouts

If you’re in the top 37% tax bracket, your itemized deductions will be reduced starting in 2026. This “phaseout” rule effectively limits how much high-income earners can deduct.

Now is the time to work with your tax advisor to explore ways to offset this change, such as deferring income, timing deductions, or restructuring your business entity.

3. Gambling Loss Limits

From 2026 onward, losses from gambling will be limited to 90% of your total losses.

Under prior law, you could deduct up to the amount of your winnings. For example:

- Old rule: $10,000 winnings and $15,000 losses → Deduct $10,000

- New rule: $10,000 winnings and $15,000 losses → Deduct only $9,000

If you frequently gamble, keep thorough records and be aware that your deductions may be smaller moving forward.

4. Mortgage Insurance Premiums Are Back

You can once again deduct mortgage insurance premiums as an itemized deduction. This can be helpful for homeowners who bought with a small down payment or refinanced under private mortgage insurance (PMI).

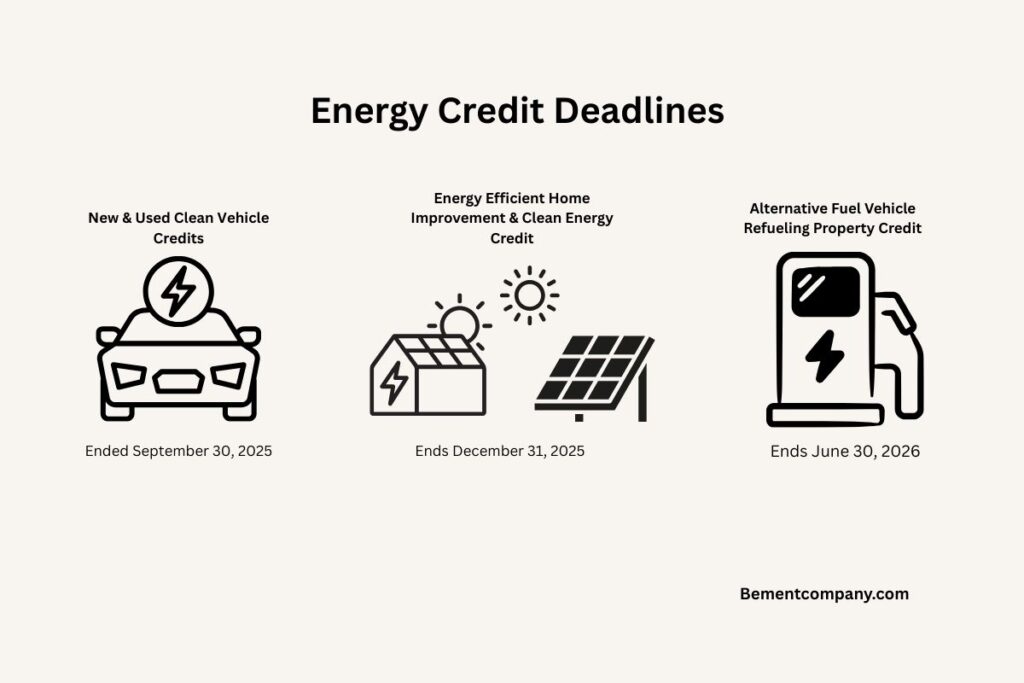

5. Energy Credits Are Expiring

Several clean energy tax credits will expire at the end of 2025, including:

- The electric vehicle (EV) purchase credit (for cars purchased after September 30, 2025).

- Residential energy-efficient property credits (for solar, windows, insulation, and appliances).

If you’re considering upgrades, make them before the deadline to maximize your benefit.

Final Thoughts

The best tax strategies are put in place before deadlines. By staying informed on what’s changing and getting organized early, you’ll make filing your 2025 return simpler and set yourself up for a smooth transition into 2026’s new tax landscape.

If you want personalized guidance on upcoming tax law changes or need help preparing your documentation, our team can help.