Have you ever wondered how some high-income earners pay little or no federal income tax?

In many cases, they’re not cheating the system; they’re using it strategically. The secret? Real Estate Professional Status.

This little-known IRS designation allows qualifying real estate investors to use paper losses from their rental properties to offset active income (like W-2 wages or business profits). When structured properly, it can mean hundreds of thousands in tax savings each year.

Let’s break down how it works, who qualifies, and how to document it correctly so you stay audit-proof.

How Real Estate Income Is Taxed

By default, the IRS classifies rental income as passive income. That means:

- Without Real Estate Professional Status:

Rental losses can only offset other passive income (like other rental profits). You can’t use them to reduce your W-2 wages or business income. - With Real Estate Professional Status:

Those same rental losses can offset all your income, including active income from your job or business.

Example:

Let’s say you earn $500,000 from your business, and your rental properties show a $100,000 loss on paper (from depreciation and expenses).

- Without Real Estate Professional Status → You still pay taxes on the full $500,000.

- With Real Estate Professional Status → You can deduct the $100,000 loss and only pay tax on $400,000.

That’s a potential savings of tens of thousands of dollars in taxes.

Learn more about passive vs active income on the IRS Rental Income and Expenses Rules page

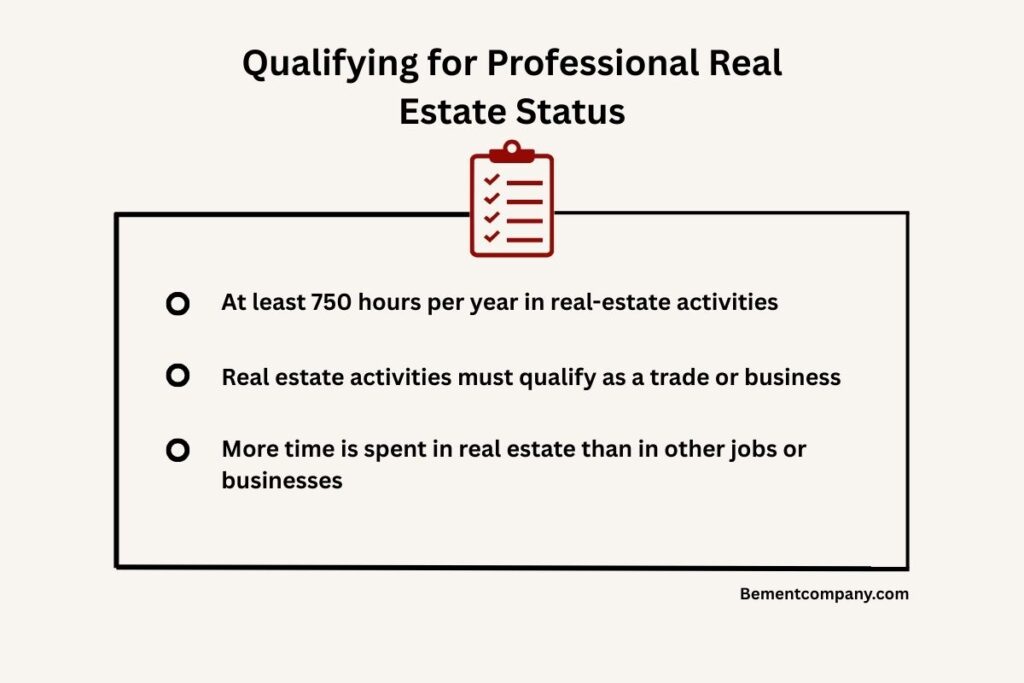

How to Qualify for Real Estate Professional Status

The IRS has strict guidelines for who qualifies. To be recognized as a Real Estate Professional, you must meet all of the following criteria:

- Work at least 750 hours per year in real estate-related activities.

These hours can include property management, renovations, tenant communications, and acquisitions. - Your real estate activities must qualify as a trade or business.

Examples include property development, construction, management, or brokerage. Simply investing in real estate without active involvement does not count. - You must spend more time in real estate than in any other job or business.

This rule can be tough for those who already have demanding full-time careers. However, if your spouse qualifies, both of you can benefit from the tax savings.

Why Spouses Are the Key to Maximizing This Strategy

If one spouse qualifies for Real Estate Professional Status, the tax benefits apply to both spouses when filing jointly.

This is a common and highly effective strategy for high-earning families where one partner manages the real estate portfolio full-time, while the other runs a business or has a high W-2 income.

Resource: Publication 924 information

Common Mistakes That Trigger IRS Audits

Because this tax rule can save so much money, it’s heavily scrutinized. Here are the most common mistakes that cause the IRS to deny Real Estate Professional claims:

- Failing to track hours: You can’t just guess or estimate. You need to log every qualifying hour in detail.

- Having another full-time job: If you claim to work 60 hours a week at your business and also 750 hours in real estate, expect questions.

- Counting unqualified activities: Researching markets or attending seminars doesn’t count toward your 750 hours. Only active management, maintenance, or decision-making does.

If you plan to claim Real Estate Professional Status, treat your recordkeeping like a second job.

Documentation You Must Keep

To stay compliant and audit-proof, maintain clear, consistent documentation. Here’s what you’ll need:

- Detailed Time Logs: Track daily real estate activities and time spent. Google Sheets or a time-tracking app works great.

- Property Management Records: Keep records of tenant communication, maintenance logs, and renovation schedules.

- Receipts and Contracts: Document every property-related expense, including repairs and professional services.

- Calendar Proof: Save meeting invites, inspection appointments, and open house schedules. These help validate your hours.

Helpful Tools:

- Property management: Stressa

- Income and Expense Worksheet: Bement Company

How Real Estate Professional Status Fits Into a Bigger Tax Strategy

This rule is powerful on its own, but when combined with other real estate tax benefits, the savings multiply.

Here are a few strategies often used alongside Real Estate Professional Status:

- Bonus Depreciation: Accelerate write-offs on new property purchases or renovations.

- Cost Segregation Studies: Reclassify property assets to shorten depreciation timelines.

- 1031 Exchanges: Defer capital gains when selling investment properties and reinvesting.

Each of these tools has specific requirements, but can dramatically reduce your overall tax liability.

Final Thoughts

Real Estate Professional Status isn’t just for full-time investors. It’s for anyone serious about using real estate to build wealth and reduce taxes.

The key is to stay compliant, document everything, and partner with an advisor who knows this playbook inside and out.

At Bement Company, our strategy team helps business owners and high earners build customized tax plans that leverage real estate and other advanced structures to keep more of what they earn.

Schedule a tax strategy session with Bement Company to find out if you qualify for Real Estate Professional Status and how it could transform your tax bill.