It is never too early to start preparing for your annual tax filing. A little planning ahead of time can help you avoid surprises, reduce stress, and uncover opportunities to save money on your taxes.

As you look ahead to filing your 2025 return, there are several important updates and planning items worth reviewing. Below is a breakdown of what is new, what has changed, and what you can still do to improve your tax outcome.

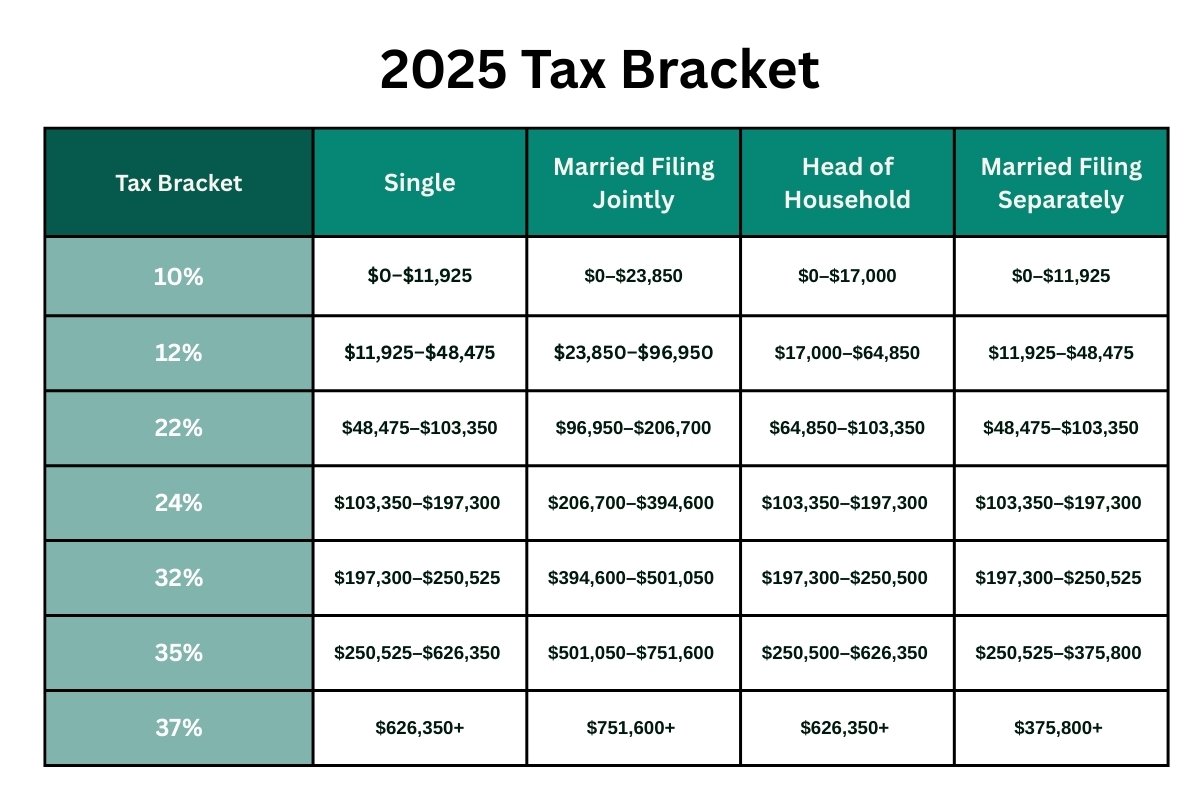

Review the 2025 Federal Tax Brackets

Your income level plays a big role in how much federal tax you owe. Even if tax rates stay the same, an increase in income could push more of your earnings into a higher bracket.

For 2025, the federal income tax brackets are as follows:

Understanding where your income falls can help guide decisions around deductions, retirement contributions, and withholding adjustments.

Claim the Child Tax Credit If You Qualify

If you have dependents under age 17 who meet IRS requirements, you may be eligible for the child tax credit.

Eligibility depends on income limits, filing status, and dependent qualifications. Reviewing this early can help ensure you claim the full benefit.

Understand State and Local Tax Deduction Limits

If you itemize deductions, you can deduct up to $40,000 for state and local taxes, or $20,000 if married filing separately. This includes state income taxes, property taxes, and personal property taxes.

For higher income earners, this deduction phases down beginning at $500,000 of income and eventually caps at $10,000. You may also elect to deduct sales taxes instead of income taxes, but not both.

For more information, check out our dedicated page to SALT / PTE Taxes

Check Your 2025 Standard Deduction

The standard deduction continues to replace personal exemptions, and the amounts increased again for 2025:

- Single filers or married filing separately: $15,000

- Married filing jointly: $30,000

- Head of household: $22,500

If your itemized deductions do not exceed these amounts, taking the standard deduction may be the better option.

Review Your Tax Withholdings

Major life changes can throw off your withholding accuracy. A new job, marriage, new child, or large bonus may result in owing money at tax time.

Reviewing your withholding now can help avoid a surprise bill or a large refund that could have been better managed throughout the year. Using tools such as a Withholding Calculator can help you estimate.

Understand the Capital Gains Exclusion on Home Sales

If you sell your primary residence and lived in it for at least two of the past five years, you may exclude up to:

- $250,000 of gains if single

- $500,000 if married filing jointly

Capital gains tax applies only to profits beyond these thresholds, calculated as the sale price minus your purchase price and qualifying improvements.

Know the Mortgage Interest Deduction Rules

For loans taken out between December 15, 2017, and December 31, 2025, mortgage interest is deductible on up to $750,000 of qualified debt, or $375,000 if married filing separately.

Interest on home equity loans is generally no longer deductible. Beginning in 2026, private mortgage insurance premiums will once again become deductible.

Review Estate Tax Exemptions

The federal estate tax exemption increased again in 2025 to:

- $13.99 million for individuals

- $27.98 million for married couples

Less than one percent of estates are subject to estate tax, but if your net worth is approaching these levels, proactive planning is essential.

Final Thoughts

Tax planning works best when it is proactive, not reactive. Reviewing these items early gives you time to adjust, plan, and make informed decisions before deadlines hit.

If you want help reviewing how these rules apply to your situation, working with a tax strategist can help you identify opportunities and avoid costly surprises.