It feels like everything costs more right now. Groceries, healthcare, insurance, subscriptions, vehicles. On top of that, companies have quietly shifted toward monthly fee models that turn everyday services into recurring expenses.

The real problem is not just inflation. It is the hidden costs in everyday spending that slowly drain your cash flow without you realizing it.

These costs are not dramatic. They are subtle. They repeat. And over time, they can add up to thousands of dollars per year.

Let’s break down the most common hidden costs and how to stop paying them.

Hidden Cost 1: Convenience Spending as the Default

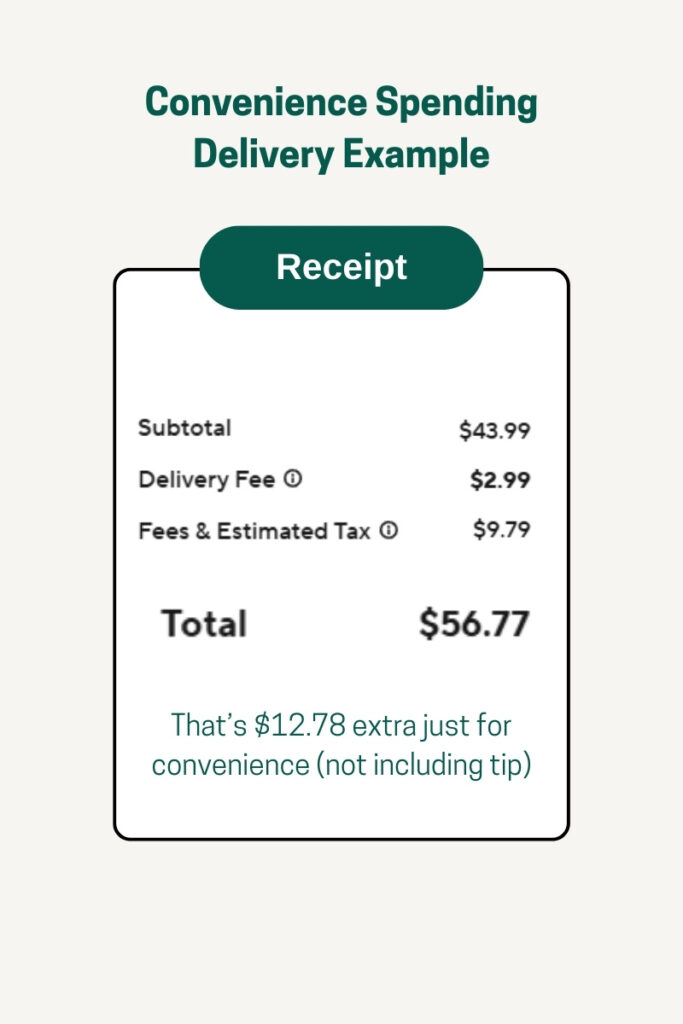

What it looks like

Convenience spending shows up as:

- Delivered meals instead of cooking

- Delivery fees and service charges

- Subscription upgrades

- Express shipping

- Same-day service add-ons

None of these purchases feels large. That is the point.

The hidden cost

The real cost is repetition. When convenience becomes the default instead of the exception, small add-ons turn into a steady monthly drain.

Ten dollars here. Fifteen dollars there. A few delivery fees per week. Over twelve months, that can easily exceed several thousand dollars.

According to the Bureau of Labor Statistics, spending on food away from home has increased significantly in recent years. That trend alone can materially affect household cash flow.

What to do about it

Start by tracking it. Do not change behavior yet. Just measure it.

Then ask:

Is this saving time or replacing a habit?

Is it occasional or automatic?

You do not have to eliminate convenience spending. The key is being intentional instead of reactive. For cash flow templates, check out our resource page.

Hidden Cost 2: Interest Expense

What it looks like

Interest shows up when:

- You carry a credit card balance

- You extend auto loans to lower the payment

- You refinance into longer terms

- You only make minimum payments

It feels manageable because the monthly payment looks small.

The hidden cost

Interest increases the true cost of everything you buy.

Credit cards are now required to show how long it will take to pay off your balance if you only make minimum payments. Many statements show that small balances can take years to eliminate.

According to Federal Reserve data, average credit card interest rates have exceeded 20 percent in recent years. That makes unpaid balances one of the most expensive forms of debt.

What to do about it

Never carry a credit card balance month to month if possible.

If you have loans, focus on reducing principal faster. Even small additional principal payments shorten the loan term and reduce total interest paid.

Internal link idea:

Link to a debt payoff strategy or tax-efficient cash flow planning post.

Hidden Cost 3: Cheap Now, Expensive Later

What it looks like

Buying the lowest-priced option because it works today.

This could apply to tools, electronics, clothing, furniture, or even services.

The hidden cost

The expense does not hit all at once. It leaks over time.

- Replacing items more often

- Paying for repairs

- Dealing with downtime

- Losing productivity

Over several years, the lower quality item often costs more than purchasing something durable from the start.

What to do about it

Ask two questions before buying:

How long will I own this?

How often will I use it?

If it is something you use frequently, quality often reduces long-term cost.

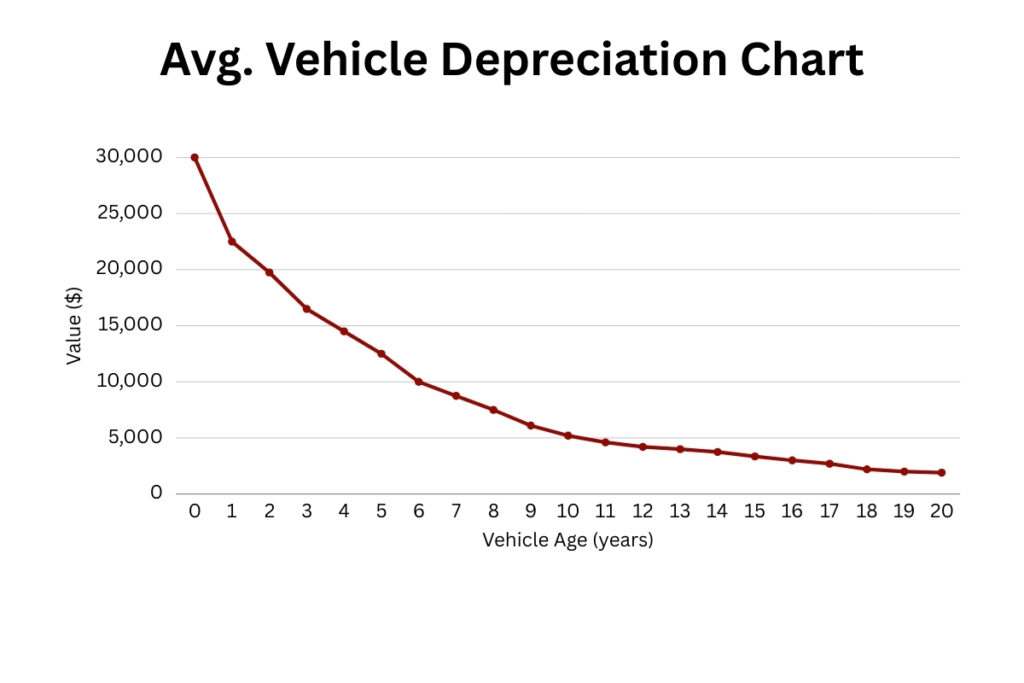

Hidden Cost 4: Vehicle Decisions That Drain Wealth

What it looks like

Buying new when slightly used would suffice

Financing a vehicle that depreciates quickly

Ignoring repair history

Purchasing highly complex vehicles with expensive parts

The hidden cost

Vehicles depreciate quickly. According to Kelley Blue Book and Edmunds data, new vehicles can lose significant value within the first few years.

If you finance a vehicle with a small down payment, you may owe more than the vehicle is worth. That creates risk if you sell or if you have an accident. It’s important to consult consumer reports on vehicle reliability.

Repair costs also vary significantly by brand and model. Some vehicles require specialized dealership repairs, increasing lifetime ownership cost.

What to do about it

Research reliability ratings before purchasing.

Favor models known for durability and repair accessibility.

Consider the total cost of ownership instead of focusing only on the monthly payment.

How to Identify Your Own Hidden Costs

If you want a practical exercise, do this:

- Review three months of bank and credit card statements.

- Highlight recurring charges and interest payments.

- Circle expenses labeled delivery, subscription, upgrade, or service fee.

- Identify anything you purchased more than once because it failed.

This exercise often reveals hidden costs immediately.

Final Thoughts

Inflation is real. Rising prices are real. But many financial pressures are not just external.

Hidden costs in everyday spending often come from habits, financing structures, and decision patterns that are within your control.

Cutting one major category of hidden costs can free up cash for:

- Retirement contributions

- Debt reduction

- Investment

- Tax-efficient planning

The goal is not to eliminate all spending. It is to spend strategically.

If you want help evaluating your cash flow, tax strategy, or entity structure to improve overall financial efficiency, explore our Tax Strategy Services at Bement Company.